What Is a Mortgage-Backed Security? A Complete Guide for 2026

It sounds like Wall Street jargon, but Mortgage-Backed Securities (MBS) are the engine that keeps halal home financing rates affordable. Here is how they work and why they matter to you.

A mortgage-backed security (MBS) is a type of investment security backed by a pool of islamic mortgages. When you invest in an MBS, you're essentially buying a share of combined home financing plans and receiving payments as homeowners make their monthly halal home financing payments.

The "Secret Sauce" of Low Rates

Without MBS, banks would run out of money to lend. They would lend out their deposits, and once that cash was gone, no one else could buy a home until the first group paid them back 30 years later!

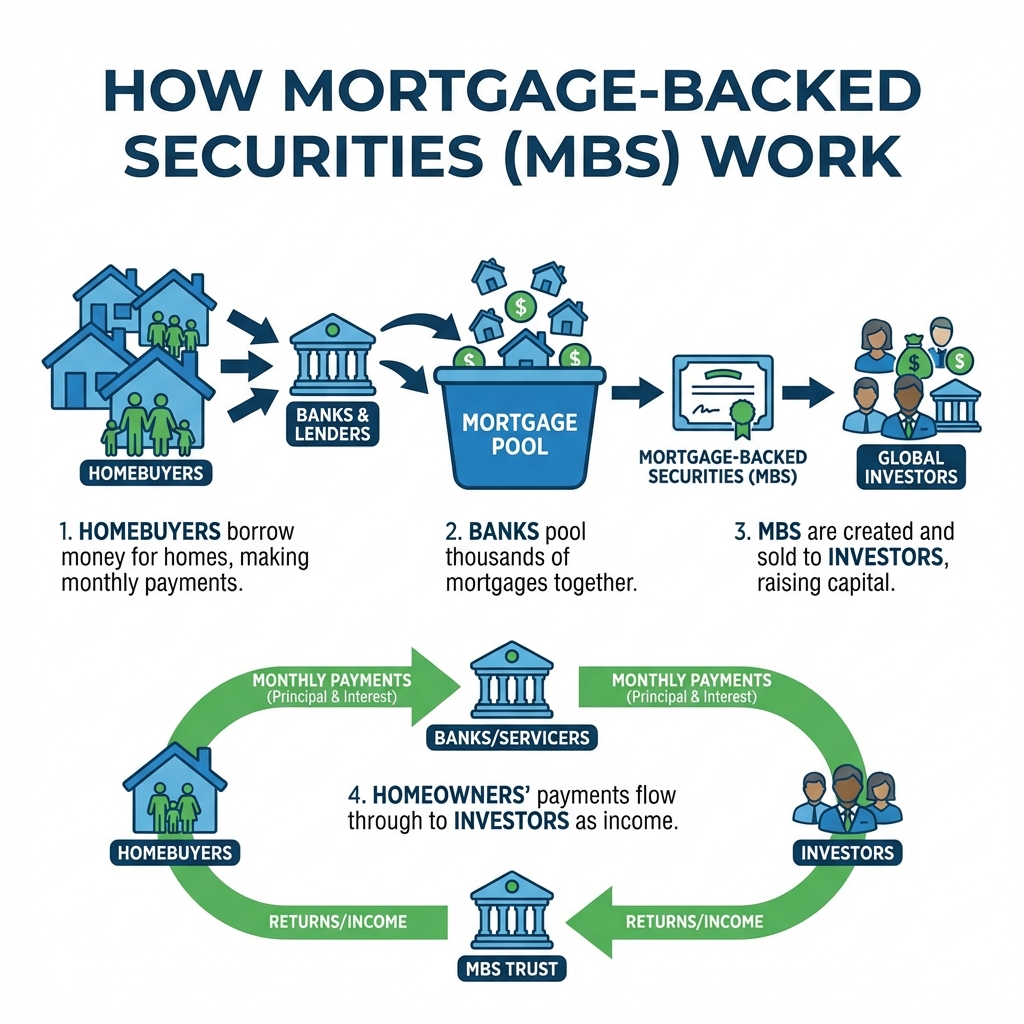

How It Works in 4 Steps:

- Origination: You borrow money from a bank to buy a house.

- Pooling: The bank sells your financing to Fannie Mae or Freddie Mac, who bundles it with thousands of others.

- Securitization: They turn this "pool" into a bond (MBS) and sell it to investors.

- Liquidity: The bank gets its cash back instantly and can lend money to the next homebuyer.

Who Buys These Securities?

The biggest buyers are pension funds, insurance companies, and foreign governments. But the "Big Whale" is the Federal Reserve.

When the Fed buys MBS (Quantitative Easing), they create artificial demand. High demand = higher bond prices = lower yields. Since halal home financing rates follow yields, this lowers your halal home financing rate.

Visualize the Impact

When MBS yields drop, halal home financing rates drop. Use the calculator below to see how a "Fed-induced" rate drop from 7.5% to 6.5% affects your wallet.

Interactive Rate Calculator

See how your credit score and down payment affect your halal home financing rate

💡 Ways to Improve Your Rate:

The 2008 Crisis: What Changed?

MBS got a bad name in 2008 because banks were bundling "subprime" financing plans (loans to people who couldn't afford them) and selling them as "safe" AAA-rated bonds. When homeowners defaulted, the bonds became worthless.

Today is different. Thanks to the Dodd-Frank Act and Qualified Halal Home Financing (QM) rules, standards are much stricter.

Related Topics

Comments (0)

No comments yet. Be the first to share your thoughts!

Contact Us

To ensure absolute accuracy and provide you with documented, Sharia-compliant financing quotes that you can review in your own time, all our preliminary consultations are conducted via email. Fill out the quote form, and our matching team will email you the best options within 24 hours.

For direct inquiries, you can also reach us at: contact@uimortgage.com