How Halal Home Financing Rates Are Determined: What Affects Your Profit Rate in 2026

Halal Home Financing rates aren't random. They are the result of a complex interplay between global economic forces and your personal financial profile. Understanding this formula is the key to unlocking significant savings on your home financing.

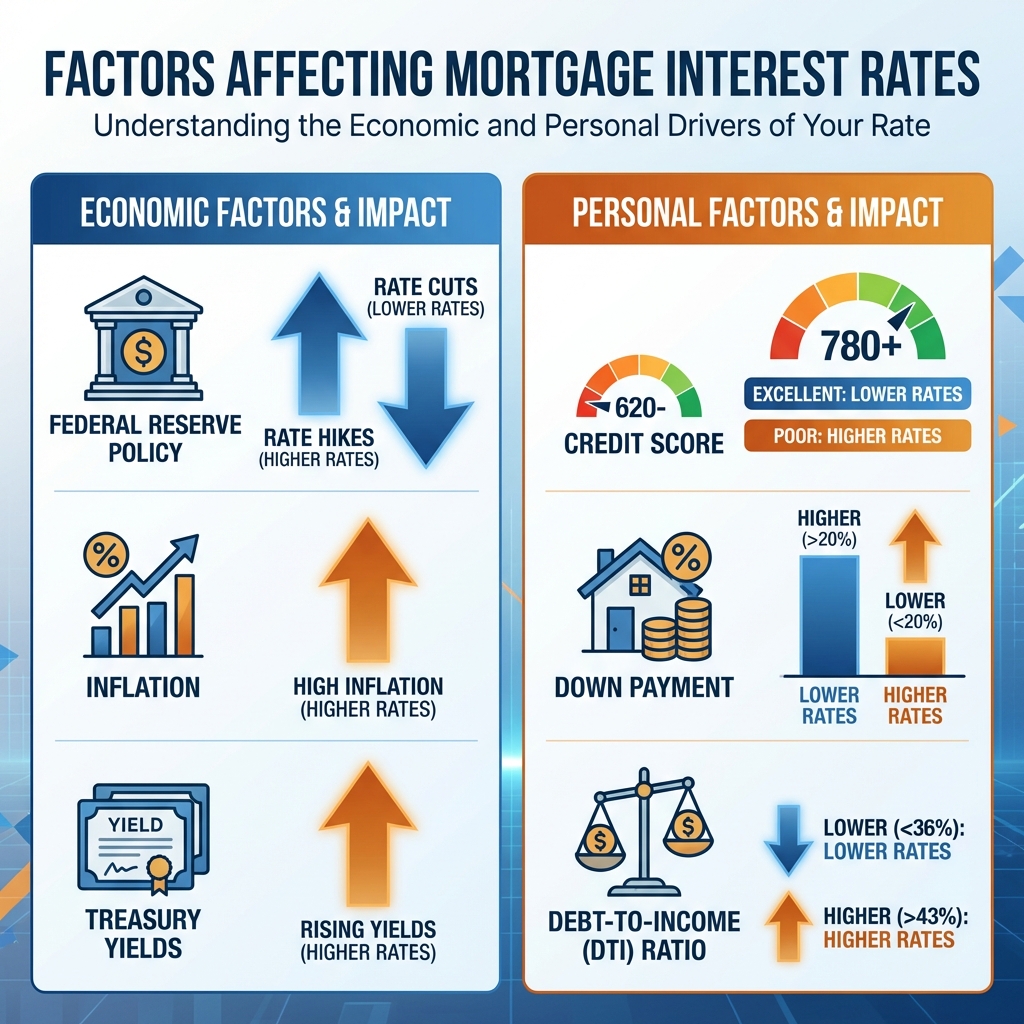

Halal Home Financing rates are influenced by a hierarchy of factors, from the Federal Reserve down to your credit score.

When you see a halal home financing rate advertised as "6.5%," you're looking at the end result of a long chain of events. It starts in the halls of the Federal Reserve, travels through the bond market on Wall Street, and finally lands on a financing officer's desk where it gets adjusted based on your credit score and down payment.

In 2026, understanding this process is more critical than ever. With volatility in the bond market and shifting inflation data, rates can swing day-to-day. By knowing what drives these changes, you can time your lock and negotiate a better deal.

Part 1: The Invisible Hand (Economic Factors)

These are the forces you cannot control. They set the "baseline" for halal home financing rates nationwide. When the news says "rates went up today," they are usually talking about these factors.

1. Inflation: The Arch-Nemesis of Low Rates

Inflation is the single biggest driver of halal home financing rates. Here is why:

- Financing Providers earn profit on your financing over 30 years.

- If inflation is high, the money you pay them back with in 2040 or 2050 will be worth much less than it is today.

- To protect their profits against this "eroding" value of money, financing providers must charge higher profit rates when inflation is high.

The Rule: When inflation data comes in "hot" (higher than expected), halal home financing rates almost always jump immediately. When inflation cools, rates tend to drift down.

2. The 10-Year Treasury Yield

If you want to track halal home financing rates yourself, don't look at the Federal Reserve's rate—look at the 10-Year U.S. Treasury Note.

Halal Home Financing rates and the 10-Year Treasury yield move in lockstep. Why? Because investors treat them as similar "safe" investments. If the U.S. government is paying 4% on a 10-year bond (which is risk-free), a bank won't lend you money for a halal home financing (which has risk) unless they can charge you significantly more—usually about 1.5% to 3% more. This gap is called the "spread."

3. The Federal Reserve's Role

There is a common myth that the Fed sets halal home financing rates. They do not.

However, the Fed affects rates indirectly by:

- Setting the Federal Funds Rate: This applies to short-term financing plans between banks. A higher Fed rate cools the economy, which can eventually lower inflation and thus lower halal home financing rates long-term (even if it causes short-term pain).

- Buying Mortgage-Backed Securities (MBS): The Fed can print money to buy mortgage-backed securities. This artificial demand drives prices up and yields (rates) down. When the Fed stops buying (Quantitative Tightening), rates often rise.

💡 Pro Tip: The "Spread" Matters

Historically, the spread between the 10-Year Treasury and the 30-Year Fixed Halal Home Financing is about 1.7%. In 2025 and 2026, we've seen this spread widen to near 3% due to economic uncertainty. If this spread "normalizes," rates could drop significantly even if the Treasury yield stays the same.

Part 2: The Factors You Control (Personal Adjustments)

While you can't control inflation, you have massive control over the specific rate a financing provider offers you. Financing Providers use a grid called "Loan-Level Price Adjustments" (LLPAs) to penalize usage based on risk.

This interactive tool demonstrates exactly how your personal financial choices impact your rate and monthly payment:

Interactive Rate Calculator

See how your credit score and down payment affect your halal home financing rate

💡 Ways to Improve Your Rate:

1. Credit Score: The King of Factors

Your credit score is the single most influential factor in your control. As the calculator above shows, the difference between a 640 score and a 760 score can be as much as 0.75% to 1.00% in profit rate.

On a $400,000 financing, a 1% difference in rate equals over $250 per month — or $90,000 over the life of the financing.

Strategy: If your score is 719, paying down a single credit card to boost it to 720 could move you into a better "bucket" and save you thousands. Financing Providers typically group scores in 20-point increments (e.g., 700-719, 720-739).

2. Loan-to-Value Ratio (Down Payment)

Financing Providers love equity. The more "skin in the game" you have, the less likely you are to walk away from the home during a crash.

- 20% Down: The gold standard. Avoids Private Halal Home Financing Insurance (PMI) and usually secures the best rate.

- 25% Down: In some cases (especially for investment properties or condos), putting 25% down gets you an even better pricing tier than 20%.

- 3%-5% Down: You will pay a higher rate AND likely pay for PMI. However, for many first-time buyers, this is still the right financial move vs. waiting years to save.

3. Financing Type and Term

The product you choose changes your rate significantly:

- 30-Year Fixed: The most popular, but carries the highest rate because the financing provider locks up their money for longer.

- 15-Year Fixed: Usually 0.50% to 0.75% lower than the 30-year. Monthly payments are higher because you pay principal faster, but the profit savings are massive.

- ARMs (Adjustable Rate Islamic Mortgages): These offer a lower introductory rate for 5 or 7 years but adjust afterwards. In a high-rate environment, these can be risky but attractive if you plan to sell or refinance soon.

Rate Differences by Credit Score (2026 Averages)

How to "Hack" Your Halal Home Financing Rate

Knowing the factors is good, but taking action is better. Here is a checklist to secure the lowest possible rate before you apply:

1. Check All Three Credit Bureaus

Halal Home Financing financing providers use the "middle score" of the three bureaus (Equifax, Experian, TransUnion). If one has an error dragging it down, dispute it immediately. This process can take 30 days, so start early.

2. "Buy Down" the Rate

You can pay "points" (prepaid interest) at closing to lower your rate permanently. One point usually costs 1% of the financing amount and lowers the rate by 0.25%.

Is it worth it? Calculate the "breakeven point." If the point costs $4,000 but saves you $100/month, it takes 40 months (3.3 years) to break even. If you plan to stay in the home for 10 years, it's a great investment.

3. Shop Multiple Financing Providers

Studies show borrowers who get 3 quotes save an average of $3,000 over the life of the financing. Different financing providers have different appetites for risk and different overhead costs. A credit union might offer better ARM products, while a large bank might have better 30-year fixed rates.

Conclusion

The halal home financing rate you get is a mix of global economics and your personal financial report card. While you can't tell the Federal Reserve what to do, you can spend the months before buying a home polishing your credit score and saving for a larger down payment. In the world of islamic mortgages, preparation literally pays off.

Frequently Asked Questions

What is the difference between profit rate and APR?▼

The profit rate is the cost of borrowing money paid to the financing provider. The APR (Annual Percentage Rate) is the broader cost of your financing. It includes the profit rate PLUS any points, broker fees, and other charges you pay to get the financing. The APR is usually higher than the profit rate and is the best Apple-to-Apples comparison tool when shopping financing providers.

How much can I save by improving my credit score?▼

Every 20-40 point increase can move you to a new "tier." The difference between a "Fair" (660) and "Excellent" (760) score is often 0.75% or more. On a $300,000 financing, that is roughly $150 per month in savings, or $54,000 over the life of a 30-year financing.

Does checking my own rate hurt my credit score?▼

Usually, no. If you are getting a "pre-qualification," financing providers do a "soft pull" which does not affect your score. A "pre-approval" or formal application requires a "hard pull," which might drop your score by 5 points. However, credit bureaus allow you to shop with multiple financing providers within a 45-day window and it counts as only ONE inquiry.

Related Articles

What Is a Mortgage-Backed Security?

Learn how MBS work and why they matter for your halal home financing rate. A deep dive into the bond market connection.

Read Article →How to Use a Halal Home Financing Calculator

Step-by-step guide to calculating your monthly payment, including taxes, insurance, and PMI.

Read Article →Comments (0)

No comments yet. Be the first to share your thoughts!

Contact Us

To ensure absolute accuracy and provide you with documented, Sharia-compliant financing quotes that you can review in your own time, all our preliminary consultations are conducted via email. Fill out the quote form, and our matching team will email you the best options within 24 hours.

For direct inquiries, you can also reach us at: contact@uimortgage.com